Sometimes, life can throw you a curveball and you find yourself in need of an infusion of cash. This could be because of illness, unemployment or a sudden need for repair or replacement of a big-ticket item. You may not have long-term savings to dip into, especially if your priority has been paying your mortgage, taxes, and utilities. You’re not ready to sell your home just yet but what if you could use your home as collateral to get that loan you need so desperately?

As a mortgage broker and financial planner, I see this situation often at a time of life, for most people, when they hoped to be looking forward to a comfortable retirement. There are a few options available to you but the two most popular ones that you may have heard about are a reverse mortgage and a home equity line of credit or HELOC. Let’s explore what each one is and which one is right for you.

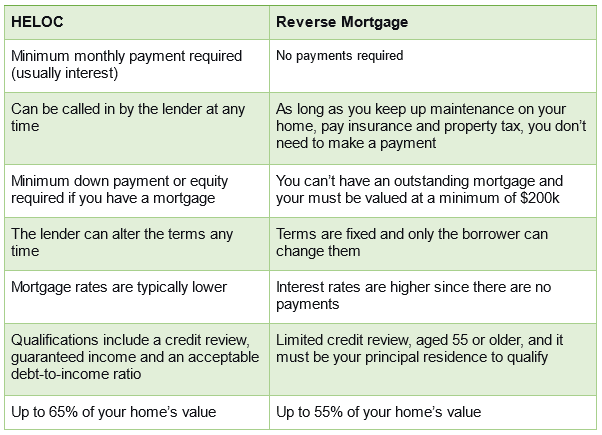

What is a home equity line of credit (HELOC)?

A HELOC lets you borrow money when you need it (up to a set amount). You only pay monthly interest on the amount you’ve borrowed and rates are lower than other lines of credit because you are backing up the loan with your home, Unlike a mortgage, there is no schedule of payments on the principal. You pay off the loan when it’s convenient for you but you must make your interest payments on time. However, if you default on your loan, you can lose your house.

What is a reverse mortgage?

A reverse mortgage provides you with either a lump sum or a large amount upfront followed by regular cash payments paid out on a schedule you choose. A reverse mortgage can be up to 55% of the market value of your home. You’ll pay monthly interest on the loan but you don’t have to make any payments until you sell the house or die. As long as you follow the terms of your mortgage, there is no risk of losing your home, and you’ll never owe more than it is worth.

Reverse mortgage vs. HELOC

If your credit is in good standing and you have a steady income, a home equity line of credit has certain advantages. For those who have a fixed income or are cash-strapped, a reverse mortgage could fit the bill. Here is an easy way to compare:

Not sure which to choose? Get an expert opinion

Either a HELOC or a reverse mortgage can help if you require funds for major or pending expenses. While selling your home or downsizing are also options, you should consult with an experienced mortgage broker. To explore your options, call me, Darren Robinson, and I’ll advise you on the best options for your situation as an experienced financial advisor. As your broker, I can make sure you understand the obligations, penalties, and what can happen to your home after your passing. I’m only a phone call away at 705-315-0516 or click here to book a virtual meeting online, to talk about which option is right for you.